As an employer, you’re required by the federal government to deduct certain taxes from your employees’ paychecks, then remit those taxes to the federal government on a regular basis. You’re also obligated to match some of those taxes and pay for others yourself.

Calculating, withholding and depositing these taxes — commonly known as payroll taxes or federal employment taxes — can be the most confusing aspect of processing payroll. The financial consequences can be high if you miss a deadline or fail to withhold the right amount.

Need help managing payroll taxes?Payroll taxes should always be paid on time to avoid any penalties. A full-service payroll software like Paycor can help you manage these taxes and take the hassle of tax compliance off your plate. |

Below, we walk you through what payroll taxes are, when they’re due and how to file them correctly.

Jump to:

Payroll tax due dates

| Income and FICA tax due dates | FUTA tax due dates |

|---|---|

|

|

Federal employment tax deposit due dates: Income and FICA taxes

Whether your federal payroll taxes are due monthly or semi-weekly depends mainly on the amount of taxes you deposit during what’s called a “lookback period.” An accountant can help you better understand which tax payment schedule your business needs to use, as can reading through the IRS’s article on employment tax due dates.

We’ll dive right into federal tax deposit due dates, but feel free to skip ahead to learn more about what a lookback period is and how to determine which schedule to follow.

SEE: The Best Payroll Software for Enterprises (TechRepublic)

Monthly tax deposit due dates

If your tax liability during the lookback period was $50,000 or less, you’ll deposit payroll taxes on the 15th of each month following the month in which the taxes were withheld.

For example, the FICA and federal income taxes you withheld from every paycheck distributed in January would be due the 15th of the next month, which would be February 15th. The FICA and income taxes you withheld in February would be due March 15th, and so on.

If this is your company’s first year in business, you’ll likely automatically default to depositing FICA and income taxes on a monthly basis. Your accountant can explain in more detail and help you determine if you need to follow this or another deposit schedule.

Semi-weekly tax deposit due dates

If your tax liability during the lookback period was over $50,000, you’ll usually deposit payroll taxes within three business days of the pay period:

- For FICA and income taxes withheld from paychecks distributed on a Wednesday, Thursday or Friday, you’ll deposit those funds the following Wednesday.

- For FICA and income taxes withheld from paychecks distributed on a Saturday, Sunday, Monday or Tuesday, you’ll deposit those funds the following Friday.

Next-day tax deposit due dates

If you have enough employees (or if you pay high enough wages) that you withheld $100,000 in income and FICA taxes on any given day during either a monthly or semi-weekly payroll schedule, you must deposit those taxes no later than the next business day.

Federal employment tax deposit due dates: FUTA taxes

How frequently you deposit FUTA taxes — which are paid solely by you, the employer, and not by your employees — depends on your FUTA tax liability over the previous quarter.

First of all, if your total FUTA tax liability was $500 or less in a given quarter, you do not need to deposit those taxes until the following quarter.

If your FUTA tax liability was over $500 in the quarter — a dollar amount that should include any FUTA taxes you didn’t deposit previously because they totaled less than $500 — you must deposit those funds no later than the final day of the first month of the next quarter.

Assuming your FUTA tax liability is over $500 each fiscal quarter, your tax deposit deadlines would be as follows:

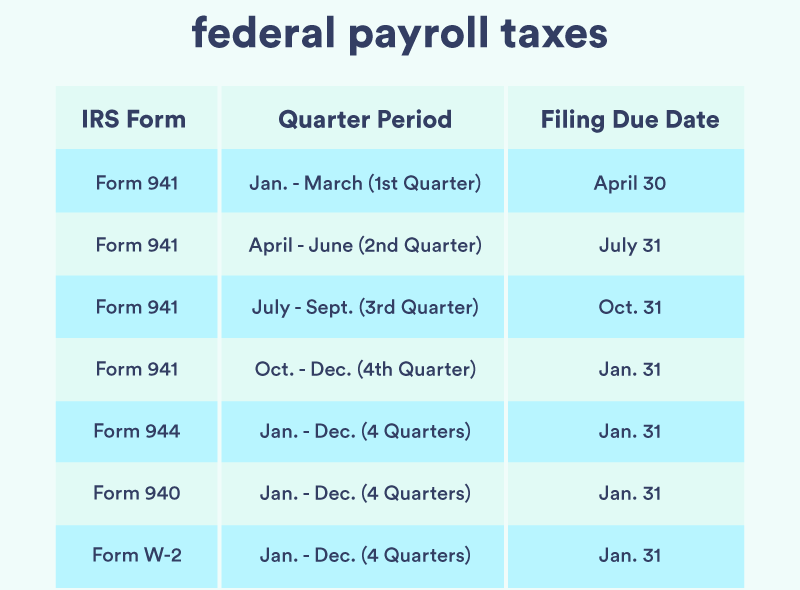

- FUTA taxes from January 1st to March 31st: April 30th.

- FUTA taxes from April 1st to June 30th: July 31st.

- FUTA taxes from July 1st to September 30th: October 31st.

- FUTA taxes from October 1st to December 31st: January 31st.

If your FUTA tax liability still doesn’t come to $500 or more by the end of the year’s final fiscal quarter, you will deposit those taxes by January 31st of the new year.

Why do payroll tax deposit due dates matter?

If you miss a payroll tax deadline, fail to deduct and file the correct tax amount or submit the wrong paperwork, you’ll likely be subject to an IRS-imposed payroll tax penalty. These penalties can include:

- Fines.

- Liens.

- Interest charged on late payments.

- Prosecution.

- Jail sentences.

Remember, these penalties aren’t imposed on employees but on the employer who failed to submit taxes correctly or on time.

The type of penalty you receive is based on how big your business is, whether the missed deadline was intentional or accidental, how late your tax payment was and how much you owe, among other factors. No matter which type of penalty you face, missing a deadline can result in major financial consequences for your business.

For instance, if you submit your federal payroll taxes late, your fine is based on how long it takes you to make the payment:

- Between one and five days late: A fine of 2% of the total late payment.

- Between six and 15 days: A fine of 5% of the total late payment.

- 16 days or more: A fine of 10% of the total late payment.

If you still don’t submit the payment within 10 days of receiving a written notice from the IRS, your tax penalty increases to a rate of 15%.

What is the Trust Fund Recovery Penalty?

The Trust Fund Recovery Penalty (TFRP) is imposed by the federal government on employers who willfully fail to withhold or remit federal employment taxes. (The “trust fund” part of the penalty stems from the fact that employers hold their employees’ taxes in trust before remitting them to the government.)

Willfully failing to remit taxes doesn’t require you to have any malicious intent. Instead, it means that you’re aware of your tax responsibilities and, for whatever reason, failed to follow through on them.

For example, if you use payroll taxes to pay off your business’s debts instead of submitting those taxes to the federal government, you’ll be considered a responsible party who willfully and intentionally misused government funds.

If the IRS notifies you that it’s assessing a penalty against your business, you have 60 days to appeal the assessment. An appeal can include demonstrating that you either aren’t the responsible party or providing evidence that you didn’t willfully fail to follow through on your tax duties. If you don’t appeal or respond to the IRS’s notification, you’ll be served with a penalty and required to make a payment.

Typically, the TFRP equals the dollar amount of tax money you failed to collect or remit, plus interest on the missed payment.

How can you avoid missing an employment tax deadline?

The IRS offers an online tax calendar that includes every employment tax deadline for any given tax year. Business owners can subscribe to an RSS feed to receive emailed notifications the week before a tax payment or tax form is due. You can also subscribe to the calendar and import it into certain calendar applications, including Microsoft Outlook.

Alternatively, payroll software usually comes with a built-in tax calendar and automatic tax deadline notifications. Self-service payroll software will calculate payroll taxes for you and notify you of crucial deadlines, but it leaves the actual fund submission up to you. Full-service payroll software both calculates and files federal employment taxes on your behalf, including the correct tax forms.

The best full-service payroll providers offer a tax penalty guarantee, meaning that if the payroll company fails to submit your taxes correctly or on time, it will pay any fee levied by the IRS on your behalf. The tax penalty guarantee does not apply to any errors made by you or your accounting and payroll team — if you don’t enter the correct paycheck amount or upload the right W-4 form, you’re responsible for any IRS fines resulting from the error.

What is a lookback period?

Put as simply as possible, a lookback period for payroll tax deposit deadlines refers to a prior, IRS-specified period of time during which you reported a payroll tax liability. Your total tax liability during the lookback period will determine whether you deposit taxes on a monthly or semi-weekly basis.

Note that lookback periods apply only to FICA and income taxes, not FUTA taxes, which have a different payment schedule.

How do you know what your lookback period is?

Look at IRS Form 941, or the Employer’s Quarterly Federal Tax Return. Most businesses with employees file this form on a quarterly basis to report their income, Medicare and Social Security taxes to the federal government. (FUTA taxes are reported and deposited on a different form and on a different cadence.)

Typically, only the smallest of small businesses use IRS Form 944 to report their income and FICA tax liability.

Form 941 filers

If you file IRS Form 941, your lookback period spans four fiscal quarters, starting on July 1st of one calendar year through June 30th of the next calendar year.

To determine their payroll tax deposit schedule for the 2023 tax year, employers who file Form 941 would look at their tax liability over four quarters’ worth of filed 941 forms:

- 2021’s third fiscal quarter, or July 1st through September 30th.

- 2021’s fourth fiscal quarter, or October 1st through December 31st.

- 2022’s first fiscal quarter, or January 1st through March 31st.

- 2022’s second fiscal quarter, or April 1st through June 30th.

Looking forward to the 2024 tax year, your lookback period would be as follows:

- 2022’s third fiscal quarter, or July 1st through September 30th.

- 2022’s fourth fiscal quarter, or October 1st through December 31st.

- 2023’s first fiscal quarter, or January 1st through March 31st.

- 2023’s second fiscal quarter, or April 1st through June 30th.

Once you’ve calculated your total tax liability over the lookback period, you can determine which payroll tax deposit schedule to follow:

- If your reported tax liability was $50,000 or less over the most recent lookback period, you must deposit federal employment taxes on a monthly basis.

- If your reported tax liability was greater than $50,000 over the most recent lookback period, you must deposit federal employment taxes on a semi-weekly basis.

Form 944 filers

If you file IRS Form 944, your lookback period spans January 1st through December 31st of a single calendar year — typically, the second-most-recent calendar year. For instance, those filing for the 2023 tax year would calculate their tax liability from January 1st, 2021 through December 31st, 2021.

Your tax deposit schedule will be based on your total tax liability over the lookback period:

- If your yearly tax liability was $50,000 or less, deposit taxes monthly.

- If your yearly tax liability was more than $50,000, deposit taxes semi-weekly.

Again, consult with your accountant for specific details on which tax forms you’re required to file, what lookback period you should use and what deposit schedule you should follow.

Payroll tax deadline FAQ

How many days after payroll are payroll taxes due?

If you deposit FICA and income taxes on a monthly basis, payroll taxes are due the 15th of the month following the month in which you distributed paychecks. If you deposit FICA and income taxes on a semi-weekly basis, payroll tax deadlines are based on payday:

- If paychecks are distributed Wednesday, Thursday or Friday, deposit payroll taxes the next Wednesday.

- If paychecks are distributed Saturday, Sunday, Monday or Tuesday, deposit payroll taxes that Friday.

FUTA taxes are due on a quarterly basis. If your FUTA tax liability comes to $500 or more over any given quarter, deposit those taxes by the final day of the new quarter’s first month.

Do I pay payroll taxes monthly or quarterly?

How often you pay payroll taxes depends on your tax liability over an IRS-defined lookback period. If you file IRS Form 941, the lookback period is the previous four quarters. If you file IRS Form 944, the lookback period is the calendar year of the second year preceding the current year (for example, look at the 2021 calendar year to determine your tax schedule for the 2023 calendar year).

If your FICA and federal income tax liability over the lookback period was under $50,000, you’ll pay payroll taxes monthly. If it was over $50,000 during the lookback period, you’ll pay taxes semi-weekly.

What happens if I pay my payroll taxes late?

Paying your payroll taxes late can result in fines, interest charges, liens on your personal property and, potentially, jail time. Avoid paying payroll taxes late by working closely with an accountant, downloading the IRS’s tax calendar or choosing payroll software that calculates and remits taxes for you.

Read next: The Best Cheap Payroll Services (TechRepublic)

Featured payroll solutions

This post originally appeared on TechToday.